Medicare Plan G Reviews 2024

- Plan G covers all of the same things as Plan F, with only one exception. While Plan F covers the Medicare Part B deductible, Plan G does not. Read our review of Plan G to see if it’s the right Medigap plan for you, too.

There will likely be a lot of Medicare beneficiaries looking for Plan G reviews in the months and years to come. That’s because recent federal legislation bars anyone who became eligible for Medicare on or after January 1, 2020 from enrolling in Medicare Supplement Plan F, which has for years been the most popular plan due to its comprehensive coverage.

If you first became eligible for Medicare after Jan. 1, 2020, you won’t be able to apply for Plan F, so the Medigap G Plan will be the type of Medicare Supplement plan that offers nearly as many benefits as Part F that you may be able to apply for if it’s available where you live. So, what is Medicare Part G, and is Medigap worth it?

In an effort to provide some guidance to incoming Medicare beneficiaries (and current Medigap beneficiaries who are considering a new Medigap plan), we’ve put together this review of Part G, covering its benefits, the leading Medicare Supplement Insurance companies and much more.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

Is Medicare Plan G Worth It?

Plan G Medicare already had the second-highest enrollment rate among all Medigap plans, even before the new Part F enrollment rule took effect in 2020. Plan G is also the fastest growing Medigap plan in terms of enrollment, with a 96% enrollment surge since 2018.

With new beneficiaries now blocked from enrolling in Plan F, Plan G is now the Medigap option offering the most comprehensive coverage to new Medicare beneficiaries, and it will likely hold the largest share of the market in the near future.

What Is the Best Medicare Supplement Plan G Company?

Like all Medicare Supplement Insurance (Medigap) plans, you may only apply for Plan G if it’s available for purchase where you live. Not all alternativess are available in all markets or from all carriers.

75% of all insurance companies that sell Medigap policies sell Plan G. Plan G is available in parts of every state and U.S. territory. There are many different insurance companies that sell Plan G, and you can use a Medigap plan finder tool or visit Medicare.gov – the official Medicare site – to view the available carriers in your zip code, such as Mutual of Omaha or Humana Medicare Supplement plans.

Some of the top Medicare Supplement Insurance companies that offer Part G according to Medicare G Plan reviews are:

What Does Plan G Medicare Supplement Cover?

There are 9 benefit areas covered by the 10 standardized Medicare Supplement Insurance plans that are available in most states, and Plan G covers 8 of those possible benefits.

Medicare Part A Deductible

Medicare Part A beneficiaries are required to meet a deductible of $1,632 for each benefit period in 2024 before Part A coverage takes effect. This means that if you’re admitted to the hospital for inpatient care, you must first spend $1,632 of your own money before your Medicare Part A benefits kick in.

It’s important to note that the Part A deductible can reset more than once in a year. You have the meet the deductible each time you have a benefit period, which starts once you are admitted for inpatient care and ends once you have been discharged and have stopped receiving inpatient care for 60 days. If you’re admitted to the hospital for inpatient care again after 60 days, however, you will be in a new benefit period and will have to meet the deductible all over again before your Pat A benefits kick in for your new hospital stay.

Plan G covers 100% of your Part A deductible costs, no matter how many benefit periods you face in a single year.

Medicare Part A Coinsurance

Part A also requires you to pay coinsurance payments beginning on day 61 of a covered inpatient stay at a hospital. Although it’s uncommon to stay in the hospital longer than 60 days, the daily costs of such a long stay could add up quickly.

Your Part A coinsurance costs are $408 per day for days 61 through 90 in 2024, and $816 per day for 60 additional lifetime reserve days. After your lifetime reserve days are used up, you’re responsible for 100% of the daily coinsurance costs.

Plan G fully covers Part A coinsurance payments along with an additional 365 days of inpatient hospital costs after all of your lifetime reserve days are exhausted.

Medicare Part B Coinsurance and Copayments

Medicare Part B requires you to pay coinsurance payments of typically 20% of the Medicare-approved amount for certain covered services and items. This can include things like doctor’s office visits or X-rays and even more potentially expensive services like cancer treatments.

Plan G covers these Part B coinsurance and copays in full.

First 3 Pints of Blood

Medicare beneficiaries are responsible for the cost of the first 3 pints of blood needed for a blood transfusion if the hospital doesn’t offer free blood from a blood bank. But Plan G covers 100% of the cost of these first 3 pints of blood, and Medigap Part B will cover the cost of any additional blood you need.

Learn More About Medicare

Join our email series to receive your free Medicare guide and the latest information about Medicare and Medicare Supplement Insurance (Medigap).

By clicking "Sign me up!" you are agreeing to receive emails from HelpAdvisor.com

Thanks for signing up!

Your free Medicare guide is on the way.

Make sure to check your spam folder if you don't see it.

Part A Hospice Care Coinsurance or Copayment

Copayments of no more than $5 may be required for drugs and other products used for symptom control and pain relief during hospice care. Inpatient respite care can also require a coinsurance of 5%. Plan G covers all of these hospice copays and coinsurance payments in full.

Part A Skilled Nursing Facility Care Coinsurance

If you have to receive inpatient care at a skilled nursing facility, Medicare Part A requires you to pay daily coinsurance payments of $204 per day for days 21 through 100 of your stay in 2024. Plan G provides full coverage of these cost requirements.

Part B excess charges

Certain health care providers are allowed to charge up to 15% more than the Medicare-approved amount for their services in what is called an “excess charge.” Plan G covers Part B excess charges in full.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

Is Plan G Medicare Covered Internationally?

Emergency care received outside the U.S. or U.S. territories is only covered by Medicare in rare circumstances. Part G covers 80% of the cost of such care, which is the maximum allowed by any type of Medigap insurance plan.

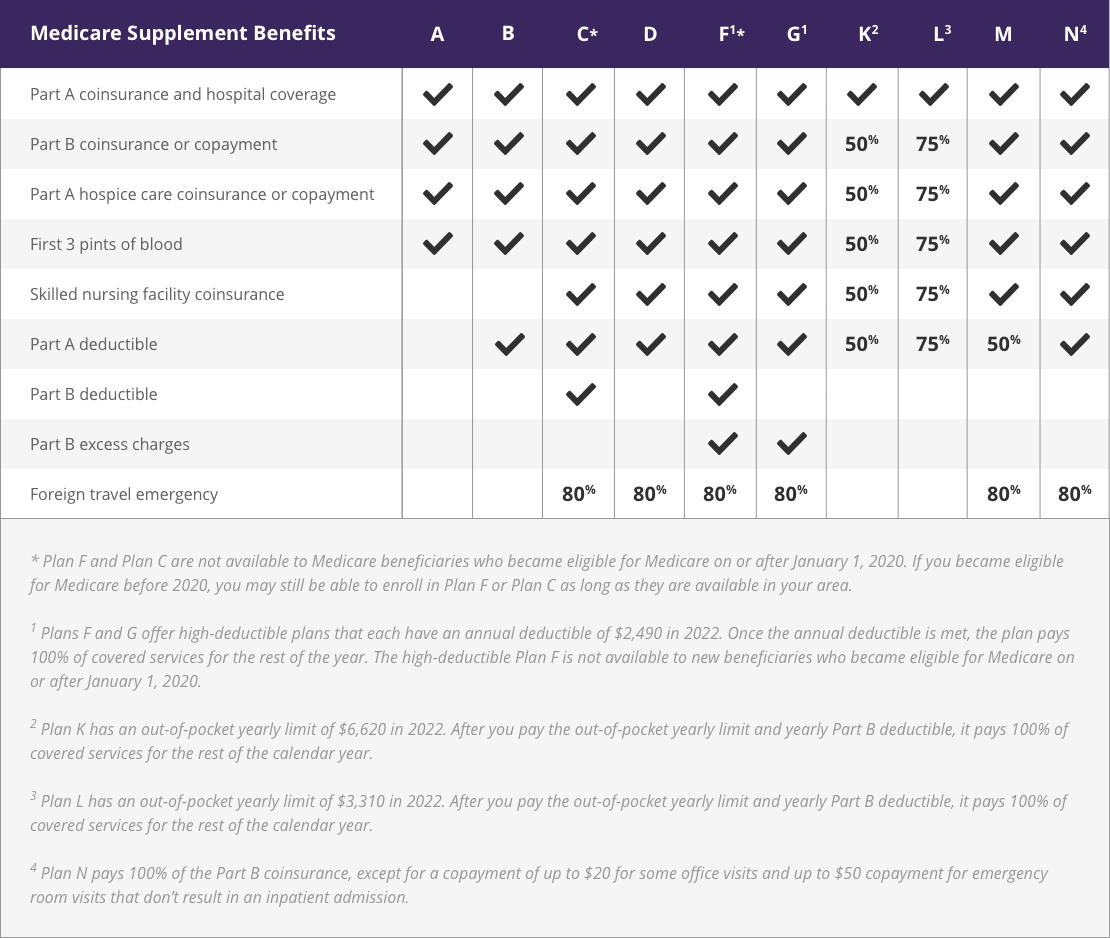

The chart below shows how Medigap Plan G stacks up against the benefits of other types of Medigap plans.

| Medicare Supplement Benefits | A | B | C1 | D | F1 | G | K | L | M | N |

| Part A coinsurance and hospital costs | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Part B coinsurance or copayment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| First 3 pints of blood | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A hospice care co-insurance or co-payment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Co-insurance for skilled nursing facility | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ | ||

| Medicare Part A deductible | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | 50% | ✓ | |

| Medicare Part B deductible | ✓ | ✓ | ||||||||

| Medicare Part B excess charges | ✓ | ✓ | ||||||||

| Foreign travel emergency | 80% | 80% | 80% | 80% | 80% | 80% | ||||

| 1. Plans C and F are not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 2. Plans F and G also offer a high deductible plan which has an annual deductible of $2,700 in 2023. Once the annual deductible is met, the plan pays 100% of covered services for the rest of the year. The high deductible Plan F is not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 3. Plan K has an out-of-pocket yearly limit of $6,940 in 2023. Plan L has an out-of-pocket yearly limit of $3,470 in 2023. 4. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 for emergency room visits that don’t result in an inpatient admission. View an image version of this table. |

||||||||||

{kind=link}

Is Plan G Better Than Plan F?

Plan G covers all of the same things as Plan F, with only one exception. While Plan F covers the Medicare Part B deductible, Plan G does not.

New Medicare beneficiaries aren’t allowed to purchase Plan F any longer because the federal government reasoned that beneficiaries who do not have to pay a deductible or any coinsurance for routine doctor’s office appointments (which are subject to the Part B deductible) might over-utilize their coverage and bog down the health care system with every runny nose and sore thumb. By forcing beneficiaries to pay the Part B deductible, they now have some “skin in the game” and may think twice before going to the doctor for minor ailments.

The Medicare Part B deductible is $240 per year in 2024, which is a smaller cost requirement than some other out-of-pocket Medigap costs.

If you first became eligible for Medicare before Jan. 1, 2020, you may still enroll in Plan F if it’s available where you live. However, it would be wise to weigh the difference in premiums between Plan F and Plan G against the cost of the Part B deductible. The $240 Part B deductible works out to roughly $19 per month.

Many people find that the higher premium for Plan F accounts for more than $19 per month more than a Plan G option in their area. In this case, you may be better off paying the lower premiums of Plan G and simply paying the Part B deductible out of pocket. That will save you money over the course of the year if you meet the Part B deductible.

What Is High-Deductible Plan G?

A high-deductible version of Plan G also exists in some areas. With this option, beneficiaries must first satisfy a deductible of $2,800 in 2024 before the plan begins covering costs. The tradeoff for the deductible is a lower monthly premium.

High-deductible Plan G may be a good option for those who want to maximize their coverage but don’t anticipate receiving a lot of care and are budgeting mostly for an emergency situation.

Have Medicare questions?

Talk to a licensed agent today to find a plan that fits your needs.

How Much Does Plan G Cost per Month?

The cost of Part G can vary within a wide range. Generally speaking, Plan G may be more expensive than other Medigap options except for Plan F since some carriers may price their offerings based on the benefits available.

In some areas, however, Plan G premiums may be lower than other Medigap plan premiums because more people are enrolled in Plan G, which may allow some insurance companies to charge lower premium costs.

Some of the variables that can factor into the price of a Medigap plan include:

- Location

Plan G sold in a major city may have higher monthly premiums than Plan G sold in a more rural part of the country, partly due to the different costs of living between the respective markets. - Carrier

Medicare Supplement Insurance is sold on the private market, where each insurance carrier is free to set their own prices to remain competitive within the market. - Age

Some carriers may charge higher rates to older enrollees or have a pricing structure that feature increasing premium costs as plan members age. - Health

If you apply for a Medigap plan outside of your Medigap open enrollment period or during any other time when you don’t have a guaranteed issue right, you may be subject to medical underwriting. Depending on your health, an insurance company may use underwriting to determine your monthly premium cost or deny you coverage altogether, which they can’t do if you apply when you have a guaranteed issue right. - Discounts

It’s not uncommon for insurance carriers to offer discounts on Medigap policies for being a non-smoker, being married or for other reasons. Be sure to ask the insurance company or your licensed insurance agent about any discounts you may be able to qualify for.

You can use the Medigap plan finder tool on Medicare.gov to get more concrete pricing details about Plan G options in your area, or you can work with a licensed insurance agent to help you find the best deal on a Plan G option near you.