Medicare

Don’t miss out on the coverage and savings you may have already earned.

What Is Medicare and What Does It Cover?

Medicare is the federal health insurance program for eligible beneficiaries in the United States. Originally enacted in 1965, the program is currently administered by the Social Security Administration, an independent agency of the federal government.

Seniors in the United States generally become eligible for Medicare benefits at age 65, or when they are diagnosed with a long-term disability at a younger age. As a rule, beneficiaries must be U.S. citizens or legal permanent residents to receive benefits.

Medicare is paid for mainly by the Social Security Administration, but its benefits are delivered in several ways, depending on beneficiaries' needs.

What Are the Parts of Medicare?

You don't need a copy of Medicare for Dummies to understand the basic division of Medicare into two main plan options:

- Publicly funded and administered Original Medicare (Medicare Part A and Part B)

- Privately sold Medicare Advantage (Medicare Part C)

Until 2006, Original Medicare consisted only of Parts A and B. Part C was introduced in 2006 as an alternative to traditional Medicare provided by private insurance companies.

Medicare also offers a prescription drug benefit called Medicare Part D. Part D Prescription Drug Plans (PDP) are sold by private insurance companies.

Millions of Medicare Part A and Part B beneficiaries also enroll in a Medicare Supplement plan (often referred to as Medigap) to help pay for out-of-pocket costs such as deductibles, copays, coinsurance and more.

What Does Part A Cover?

Medicare Part A covers most inpatient services, including:

- Inpatient care in a hospital

- Skilled nursing facility care

- Short-term care in a post-acute nursing home facility, but not long-term care or assisted living

- Hospice services

- Home health care

Part A can cover hospitalization costs if you're admitted to a hospital on a doctor's order, the hospital accepts Original Medicare and the hospital administration approves your stay.

For benefits purposes, Medicare counts all of these facilities as inpatient hospitals that are generally eligible for payment:

- Acute-care hospitals

- Long-term care hospitals

- Critical-access hospitals

- Inpatient rehabilitation facilities

- Inpatient psychiatric facilities

- Inpatient care delivered as part of an approved clinical study

During your stay in a qualifying facility, Part A benefits include the daily charge for inpatient care, plus the assorted extra costs of care while you are a patient. These include:

- Shared and semi-private rooms

- Meal service, including special diet meals and snacks

- Registered nursing services

- Drugs administered as part of your regular treatments

- Medical services, supplies and other miscellaneous costs incurred as part of your stay

How Much Does Part A Cost?

Medicare beneficiaries who worked and paid Medicare taxes for at least 40 quarters (10 years) get Part A benefits without paying a monthly premium.

If you didn’t work long enough to qualify for premium-free Part A, your Part A premium could be $278 or $505 per month in 2024, depending on how long you worked and paid Medicare taxes.

While Part A does not charge a monthly premium for most of its beneficiaries, there are other out-of-pocket costs. Part A beneficiaries must meet a Part A deductible for each benefit period. In 2024, the Part A deductible is $1,632 per benefit period.

The Part A deductible is not annual, and you could potentially face more than one benefit period in a calendar year. The benefit period that the Part A deductible applies to starts when you are admitted for inpatient care, and it ends once you have been discharged and stopped receiving inpatient care for 60 consecutive days.

- For example, consider you are admitted for inpatient hospital care on June 1 and are released on June 8, and you are then readmitted for inpatient care again on June 15.

- Because you are still in the same benefit period, you wouldn’t need to hit your Part A deductible again before your benefits kick in.

- If you are discharged on June 8 and are readmitted for inpatient care in October of the same year, you would be in a new Part A benefit period.

- This means you would have to meet your Part A deductible again, even if you reached your deductible during your June hospital stay.

In addition to the deductible, Part A benefits carry a coinsurance requirement.

- During the first 60 days of treatment, the coinsurance amount charged is $0.

- During days 61 through 90, the cost rises to $408 each day for the benefit period in 2024.

- On day 91 and beyond, the cost is $816 a day for up to 60 lifetime reserve days.

Beneficiaries are allotted a maximum of 60 lifetime reserve days that may be used after the 90-day allowance per benefit period. These 60 days are never replaced. Once the lifetime reserve days are exhausted, beneficiaries are responsible for the entire daily cost of hospitalization.

What Does Part B Cover?

Part B typically covers costs for:

- Medically necessary services and supplies needed to diagnose or to treat a medical condition. This includes diagnostic testing in many cases, as well as durable medical equipment (DME) and some other medical supplies.

- Preventive services, including routine checkups and diagnostic office visits. In most cases, preventive care is free at the point of service if the provider accepts Medicare assignment.

- Limited outpatient drugs. These include some vaccinations, IV antibiotics and other prescription medications that are typically dispensed in a clinical setting. Part B does not pay for retail drugs you pick up at a pharmacy.

- Limited mental health care, including non-residential drug and alcohol rehabilitation services and outpatient clinical observation.

- Both emergency and non-emergency medical transportation, provided the non-emergency transportation is provided by a BLS/ALS/Critical Care ambulance service that accepts Medicare, and the ride has been authorized by a physician as medically necessary.

- Some clinical research, such as experimental drug trials and disease research. This can include Alzheimer's research and some experimental therapies for dementia.

How Much Does Part B Cost?

Part B coverage comes at a monthly cost for beneficiaries. Congress adjusts the premiums, deductibles and copayment amounts charged under Medicare Part B each year as part of its annual adjustment of the Social Security Act.

In 2024, the standard monthly premium for Part B is $174.70.

Since 2007, Part B premiums have been adjusted upward for beneficiaries who earn income significantly higher than the national average. This is called the income-related monthly adjustment amount (IRMAA).

- Single seniors who receive Medicare Part B coverage and filed 2022 taxes with a reported income of $103,000 or less a year – or $206,000 for married couples filing jointly – pay the standard 2024 premium of $174.70 per month.

- Above that level, beneficiaries' premiums rise with income to a maximum monthly cost of $594 for those who earned more than $500,000 a year as single income tax filers in 2024, or $750,000 a year as married couples filing jointly.

If you receive retirement benefits from Social Security, the Railroad Retirement Board or the Office of Personnel Management, your Part B premiums may be deducted from your monthly retirement benefits check.

For beneficiaries who don’t receive retirement income from these sources, the Social Security Administration may send a monthly bill for Part B premium costs.

In addition to the premium beneficiaries must pay, the annual Part B deductible in 2024 is $240.

After you reach your annual deductible, you typically pay 20% of the cost for your covered Part B goods and services for the rest of the year, with the other 80% paid for by Medicare.

What Do Medicare Advantage (Part C) Plans Cover?

Medicare Advantage (Medicare Part C) plans essentially replace your Part A and Part B coverage with a plan provided by a private insurance company who is reimbursed by the federal Medicare program for covering you.

By law, all authorized Part C plans must include the same benefits as Medicare Parts A and B, though many plans include extra coverage for services not traditionally covered by Medicare, such as dental and vision care.

In addition to Part A and B services, many Part C plans can also cover things like:

- Prescription drug coverage

- Dental care

- Hearing and vision care, often including eyeglasses and hearing aids

- Transportation

- Home meal delivery

- Over-the-counter (OTC) items

- Telehealth

The types of plans available and the benefits they offer can vary considerably between companies, states and sometimes geographic areas of states.

How Much Do Medicare Advantage Plans Cost?

Medicare beneficiaries who opt into Part C typically pay a monthly premium for their Medicare Advantage plan. There are, however, many Medicare Advantage plans that feature $0 premiums. If you have a $0 premium Medicare Advantage plan, you are typically required to continue paying your monthly Part B premium.

Medicare Advantage plan deductibles, copays, coinsurance and other costs vary from one plan to the next. All Medicare Advantage plans are required to include an annual out-of-pocket spending limit, which helps protect you from potentially skyrocketing out-of-pocket costs. Original Medicare doesn't include this type of spending limit, which can leave you vulnerable to potentially high costs.

In 2024, the maximum out-of-pocket (MOOP) amount for Medicare Advantage plans is $8,850. Some plans may offer a lower out-of-pocket limit.

What Types of Medicare Advantage Plans Are There?

Though details of each plan vary, Medicare Advantage plans typically come in one of the following four plan types:

- Health maintenance organization (HMO)

Under an HMO plan, beneficiaries get most of their care from doctors and health care providers who are part of the plan network. Most beneficiaries have one primary care physician who can direct their care and whose referral is usually needed for specialist visits or special diagnostic tests.

You may be able to get some health care services outside of your HMO plan network, but you will generally pay higher out-of-pocket costs if you do. You could even wind up paying 100% of the price for out-of-network care. While this is seen as a negative for some people, other beneficiaries may appreciate the coordinated care offered by an HMO. HMO plans also typically feature lower monthly premiums and other costs than other types of Medicare health plans. - Preferred provider organization (PPO)

PPO plans are similar to HMOs, but they have more flexibility built into them.

PPO plans include networks of preferred medical providers. Beneficiaries are generally free to seek out in-network practitioners they are comfortable with but may also be able to also visit non-network doctors and providers. You typically pay lower out-of-pocket costs if you visit an in-network doctor or provider, however.

Specialist visits and extra testing can often be arranged without prior approval, which is different from most HMO plans.

Many PPOs pay some or all of the cost of emergency care, regardless of where it is obtained, and plans generally have a provision for beneficiaries who need non-emergency care while traveling in an area not served by the network. Out-of-network care typically costs more than care received in the plan network. - Private fee-for-service (PFFS)

PFFS health plans are designed to be as flexible as possible. With PFFS coverage, beneficiaries are free to find their own providers, though the policy only pays hospitals and practitioners who accept the plan rules and reimbursement policies.

For care delivered by an approved provider, point-of-service costs are paid as with any other health insurance. For services performed by a non-plan practitioner, seniors may have to pay some or even all of the costs they incur. - Special needs plans (SNP)

A Medicare SNP is a type of Medicare Advantage plan that's tailored to meet the needs of specific beneficiaries, such as people with chronic conditions who require specialized care or beneficiaries who qualify for both Medicare and Medicaid.

Flexibility is minimal for most SNPs, which frequently lock in specific providers to deliver care. Specialist care for seniors with diabetes, HIV, limitations caused by stroke or other disabilities can be very expensive for many seniors, but the tailored care a typical SNP pays for can make those costs lower than a more general care plan is likely to provide.

Beneficiaries who are eligible for both Medicare and Medicaid are considered “dual eligible.” These beneficiaries may have the opportunity to enroll in a type of SNP called a D-SNP.

What Does Part D Cover?

Part D is an optional Medicare prescription drug benefit. Medicare Part D prescription drug plans are provided by private insurance companies, and you can purchase either a standalone Part D prescription drug plan (PDP), or you can get Part D coverage included in a Medicare Advantage plan. These types of plans are called Medicare Advantage Prescription Drug Plans (MA-PD).

Providers are allowed to build some flexibility into the coverage they offer, though all authorized providers must meet certain minimum standards for drug costs, care and coverage.

How Much Does Part D Cost?

Part D plans organize the drugs they cover into groups called tiers. Which drugs are covered, what they cost and how they are paid for can change depending on the tier the specific drug is assigned to within your plan.

These tiers are part of a Part D plan formulary, which is the list of drugs covered by the plan. Drug formularies can change from one Medicare Part D to the next.

Generally, the Part D tiers are:

- Tier 1: This is the lowest tier of covered prescriptions. Drugs in this category include most generic prescription medications, and they carry the lowest copayment among covered drugs.

- Tier 2: Preferred brand-name prescription drugs are classed as tier 2. The copayments for these drugs tend to be higher than for tier 1 generics, but prices are still intended to be easily manageable for most seniors.

- Tier 3: Tier 3 is for non-preferred brand name drugs that have less coverage than the two previous tiers. Drugs in this category incur significant out-of-pocket costs, and it is generally worthwhile to ask about a generic or preferred alternative.

- Specialty tier: Prescription drugs in the specialty tiers tend to be very expensive at the point of delivery. Some of the newest and most effective drugs are in this category, where copayments are highest. Many experimental drugs are classified as specialty tier by Medicare.

Many Part C Medicare Advantage plans include a prescription drug benefit as part of their regular coverage. It is very important that beneficiaries check whether their Part C plan has this coverage. Beneficiaries who are enrolled in Medicare Advantage plans that lack prescription coverage may be able to add a Part D plan to their health insurance package, as long as they sign up during specific Medicare enrollment periods.

Costs for Part D plans vary by location and by the plan carrier, but all are constrained by a maximum limit for the annual deductible. In 2024, this limit is $545 a year. Authorized Part D plans are allowed to charge less than this amount as a deductible, and some carry no deductible at all.

Prior to 2020, Medicare Part D plans had a gap in coverage known as the "donut hole," as a result of the non-overlapping levels of insurance they offered. The donut hole officially closed in 2020, but beneficiaries may still have to pay a somewhat higher copayment for certain drug costs when they reach that phase of drug coverage.

Part D coverage amounts fall into three main baskets: initial coverage, the donut hole and catastrophic coverage.

- Initial Coverage

Part D initial coverage starts at the $0 mark and rises to $5,030 in total costs for prescriptions in a single year in 2024. In this window, your copayment and deductible varies according to the plan you have, but copays are generally low.

Above the initial coverage limit, beneficiaries must pay a fraction of the cost of drugs. - Donut Hole

Once the initial coverage limit is reached, beneficiaries pay a copayment of no more than 25% of the base cost of generic and brand name drugs. After that, Part D steps in to pay the remaining 75%. This continues until a catastrophic care threshold is reached. - Catastrophic Coverage

Catastrophic coverage begins when a Part D beneficiary spends more than $8,000 out of pocket in 2024.

Note that this is the amount a beneficiary personally pays, not the total cost of medications paid by all parties together. Above the catastrophic threshold, beneficiaries pay only a small copayment or coinsurance amount for all prescriptions thereafter.

Seniors who meet certain income and asset limitations (which are roughly in line with the standards for receiving SNAP and Medicaid benefits ) may qualify for prescription cost assistance through Medicare Extra Help.

Extra Help, also known as the Part D Low-Income Subsidy (LIS), is a federally funded assistance program that kicks in at the initial coverage threshold to prevent a coverage gap. Beneficiaries enrolled in Extra Help pay no additional costs inside of the donut hole.

What Does Medicare Supplement Insurance (Medigap) Cover?

Original Medicare has some gaps in coverage such as copays, coinsurance, deductibles and more. Many Medicare beneficiaries choose to plug some of those gaps with a Medicare Supplement plan, also known as Medigap. Medigap policies help pay for many of the remaining costs Original Medicare leaves unpaid.

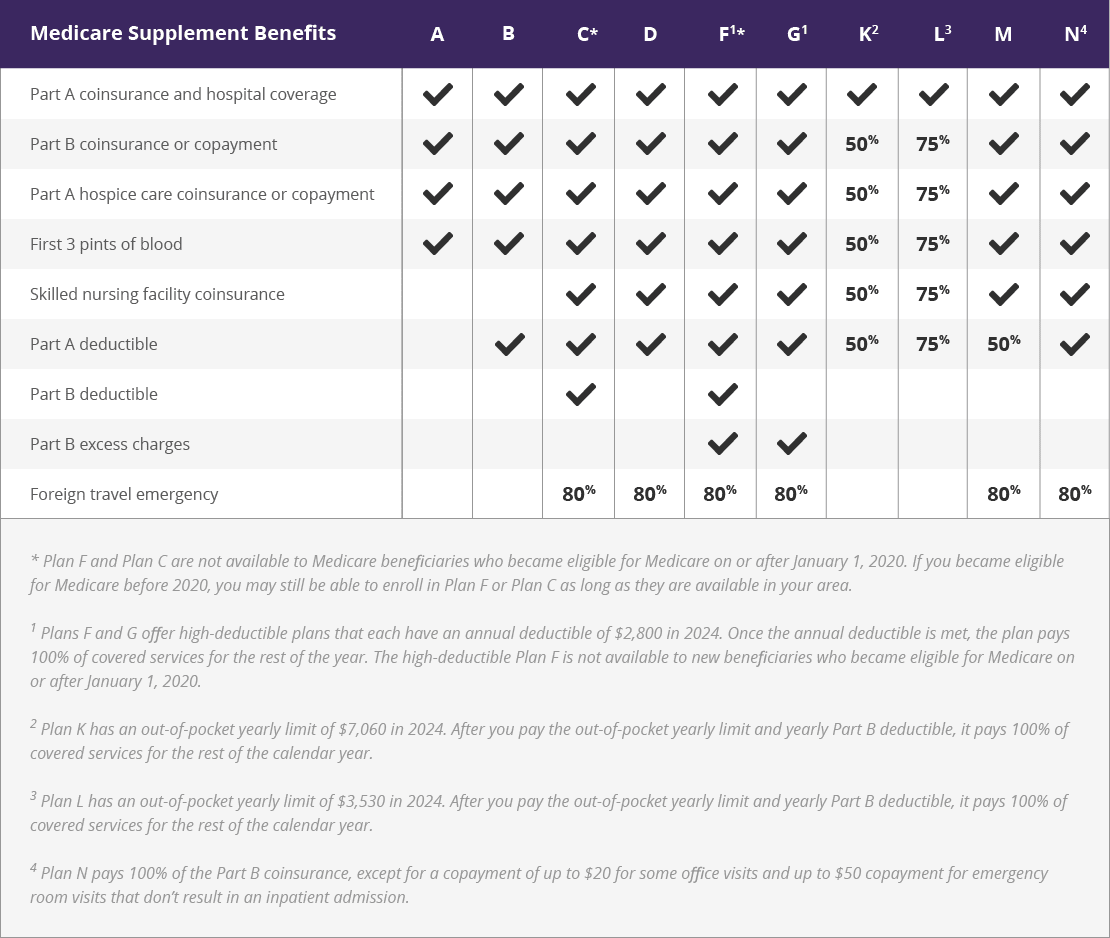

There are 10 federally standardized Medicare Supplement plans available in most states. Wisconsin, Massachusetts and Minnesota standardize their plans differently. The 10 standardized plans have lettered plan names.

| Medicare Supplement Benefits | A | B | C1 | D | F1 | G | K | L | M | N |

| Part A coinsurance and hospital costs | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

| Part B coinsurance or copayment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| First 3 pints of blood | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Part A hospice care co-insurance or co-payment | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ |

| Co-insurance for skilled nursing facility | ✓ | ✓ | ✓ | ✓ | 50% | 75% | ✓ | ✓ | ||

| Medicare Part A deductible | ✓ | ✓ | ✓ | ✓ | ✓ | 50% | 75% | 50% | ✓ | |

| Medicare Part B deductible | ✓ | ✓ | ||||||||

| Medicare Part B excess charges | ✓ | ✓ | ||||||||

| Foreign travel emergency | 80% | 80% | 80% | 80% | 80% | 80% | ||||

| 1. Plans C and F are not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 2. Plans F and G also offer a high deductible plan which has an annual deductible of $2,800 in 2024. Once the annual deductible is met, the plan pays 100% of covered services for the rest of the year. The high deductible Plan F is not available to new beneficiaries who became eligible for Medicare on or after January 1, 2020. 3. Plan K has an out-of-pocket yearly limit of $7,060 in 2024. Plan L has an out-of-pocket yearly limit of $3,530 in 2024. 4. Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to $50 for emergency room visits that don’t result in an inpatient admission. View an image version of this table. |

||||||||||

{kind=link}

Medicare supplemental plans are offered by authorized private insurance companies. Each provider is licensed on a state level to offer designated Medigap policies.

Laws for what's included in a Medigap policy, what it costs and how the member pool is managed vary between states. As a rule, applicants join a Medigap pool that is open only to eligible beneficiaries in their state, or their region of a large state. Plans are geared toward the providers available in the area, so costs and coverage limits vary.

By law, no senior who is eligible for Medicare may be refused coverage by a Medigap policy because of a preexisting condition, as long as they apply for a plan during a period in which they have a guaranteed issue right.

Guaranteed issue rights may be granted for a number of situations such as:

- You lose your previous Medigap coverage through no fault of your own, such as the plan no longer being offered in your area

- You move to a new area where your current Medigap plan is no longer offered

The most common guaranteed issue right is when you apply for a Medigap plan during your Medigap Open Enrollment Period. This is the best time to apply for a Medicare Supplement plan.

- Your Medigap Open Enrollment Period begins as soon as you are at least 65 years old and are enrolled in Medicare Part B.

- Your Medigap Open Enrollment period lasts for six months.

- During this period, a Medicare Supplement Insurance company cannot deny you coverage or charge you more for a Medigap policy due to your health.

If you apply for a Medigap policy during a time when you don’t have guaranteed issue rights, the insurance company may require you to undergo medical underwriting. This means that the company could charge you more for your policy – or deny you coverage altogether – based on your health.

Important Resources

You can complete a number of necessary Medicare steps and find additional information by visiting some of the official government websites listed below. Some of our resource guides and expert articles help further explain some of the information you’ll find on these sites.

Read Our Featured Guides

Answer questions such as "When is Medicare Open Enrollment?" or "How do I enroll in 2024 Medicare?" Don't miss certain Medicare enrollment period deadlines, or you may be subject to higher costs, late enrollment penalties or lapses in coverage.

Medicare Advantage plans, also known as Medicare Part C, replace your Original Medicare coverage and can provide extra coverage. We break down the best Medicare Advantage plans in 2025 from top insurance companies.

Find and compare 2024 Medicare Advantage (Part C) plans and Medicare Supplement (Medigap) plans available where you live. Select your state to find out more about Medicare plans near you and learn how to sign up for Medicare in your state.

This chart comparing Medicare Supplement (Medigap) plans outlines the benefits of each of the 10 different standardized Insurance plans available in most states. Compare plans to learn what’s covered.